iögo

Events, Seasonal and Short-Term (GOLD)

Client Credits: Aliments Ultima

Lucie Rémillard, Vice President, Marketing, Ultima Foods Inc.

Chantale Sévigny, Brand Group Director, Ultima Foods Inc.

Hélène Boidin, Brand Group Director, Ultima Foods Inc.

Geneviève Bibeau, Brand Manager, Ultima Foods Inc.

Lynda Lamontagne, Brand Manager, Ultima Foods Inc.

Nathalie Gamache, Director, Innovation and Process, Ultima Foods Inc.

Anita Lepage, Director, Marketing Research, Ultima Foods Inc.

Diane Jubinville, Director of public relations and consumer relations, Ultima Foods Inc.

Agency Credits: DentsuBos

Claude Larin, Vice President, Brand Strategy, DentsuBos

Roger Gariépy, Hugo Léger, Vice President, Creative direction, DentsuBos

Ron Caplan, Copywriter, DentsuBos

Samatha Hull, Jeffery Rosenberg, Art directors, DentsuBos

Camille Forget, Sarah Gervais-Houle, Designers

Francois Mailloux, Vice President, Client services, DentsuBos

Marlène Chapelain, Account Director, DentsuBos

Frederic Rondeau, Vice President, Media, DentsuBos

Véronik L’heureux, Alex Guimond, Media planners, DentsuBos

Rebecca Rodrigues, Renée Petranic, David Wicken, Media buyers, DentsuBos

Section I — BASIC INFORMATION

| Business Results Period (Consecutive Months): | Mid August-Mid November 2012 |

| Start of Advertising/Communication Effort: | Mid August |

| Base Period as a Benchmark: | This case is about a new product |

Section II — SITUATION ANALYSIS

a) Overall Assessment

The story that led to the birth of the iögo yogurt brand is unique. After searching for a comparable case in the business world, we realized that nothing resembles it.

Imagine: your company is called Ultima Foods. During the past 40 years, you’ve created Yoplait’s success across Canada. You’ve built strong blockbuster brands like Minigo, Yop, Tubes and Source. At the end of 2011, your business employs 750 people and you run world-class facilities. Your annual revenue has reached $330 million and grows every year. Your share of the Canadian yogurt market is close to 30%, and you own the 2nd most important market share next to Danone (36%). And this share is twice the size of your closest challenger, Parmalat (Astro), who holds 13%. [Footnote #1]

Then one day, you suddenly learn that your Yoplait license contract will not be renewed. The French and the American owners of the Yoplait brand – Sodiaal and General Mills – have decided to stop their licensing activities and their plan is to fully integrate their operations in Canada. They’ll be taking possession of your Yoplait assets in a few months (listings, labels, advertising material, website, etc.)

During this operation, everything will continue on for Yoplait. The consumer will see no changes on the shelves. Product availability will be the same. For Ultima Foods however, this will represent an abrupt change, and up to a 95% drop in business.

For the future of the company and its 750 jobs, and for the stakeholders who have the intention to remain a Canadian yogurt industry leader, you’ll need to launch a new national yogurt brand from scratch. A strong brand with the muscle needed to compete with the international giants in the category, and able to obtain an important market share rapidly. You have 18 months to invent a brand, develop a full product portfolio with recipes and packaging, prepare for product introduction (with all retailers across the country), and proceed with your launch activities.

But re-entering the market as a completely new player is not an easy thing to do.

In the yogurt industry, the competitive pressure is high. In the past, yogurt sales were growing in double digits year after year. But since 2009, growth has slowed down to a yearly 5% average [Footnote #2]. The main product categories (0%, Probiotic, Tubes, Fresh Cheese) are not growing anymore. Gaining and retaining consumers requires more marketing investments. This explains why brands like Activia, Source, Silhouette, Astro, Minigo, Danino, and Tubes have invested over 45M$ year over year in advertising, battling for consumer preference and share of voice.

Building a new brand through all this advertising noise will require more than a good media buy.

Finally, adding to the barriers in the market is the fact that the national leading yogurt brands have also made the consumer accustomed to regular price reductions. In Canada, yogurt is being sold on sale half of the time.

b) Resulting Business Objectives

After the first months of intense creative work, a fresh brand name came up and scored high in consumer research: ‘iögo’. Short and different. With a strong signature line that adds a nice dimension to the name: ‘iögo. The new way to say yogurt’. A promising and solid start.

For a company the size of Ultima Foods, iögo’s national sales would need to be high right from the start. iögo had to become a challenger against the top tier brands within the 1st year. Market share objectives were set at 8% (minimum)—close enough to the 3rd and 4th positions held by Astro (13%) and Liberté (11%) [Footnote #3]. Ultima would achieve this objective by successfully launching a portfolio of 44 different products for grocery stores and 21 products for food service accounts on day one.

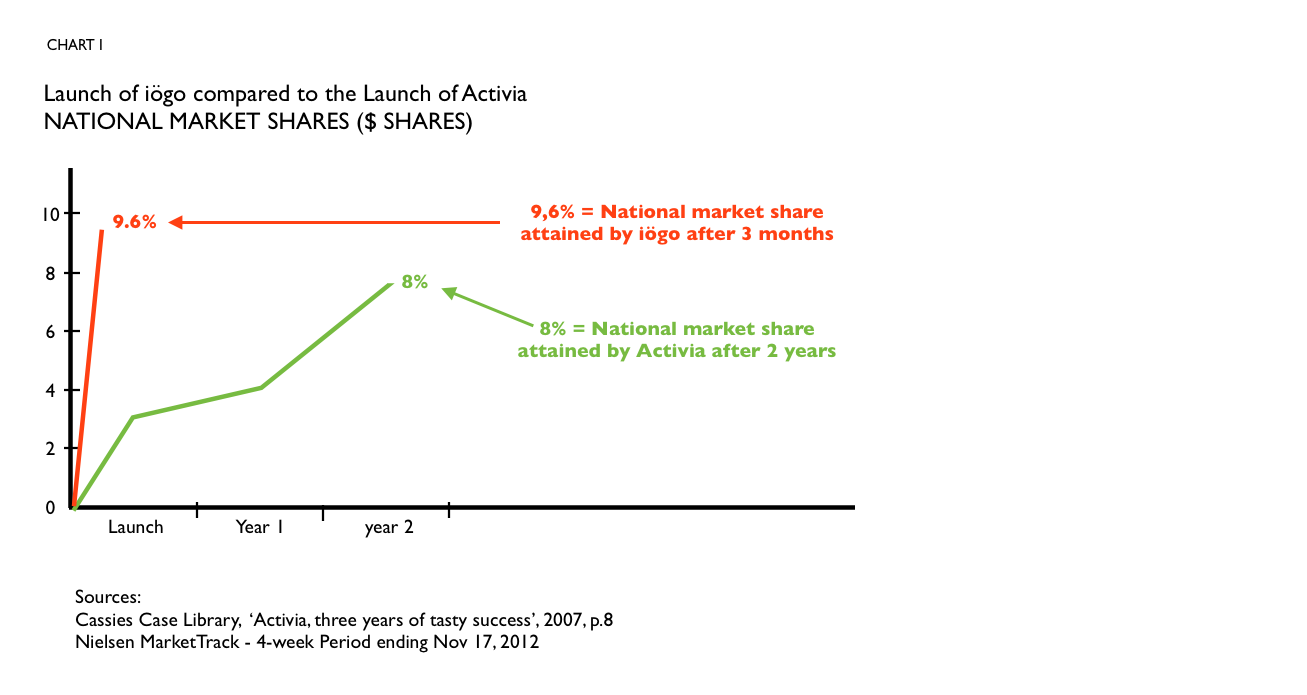

We needed a strong and convincing plan, along with results from day one of the launch to make sure retailers would support iögo for the long run. The last major success in Canadian yogurt history was the launch of Activia in 2004. It had managed to gain an 8% market share in over 2 years, with total awareness levels of 56% across Canada. Its market share had then risen to 14.9% after its third year. [Footnote #4]. To reach its objective, iögo would have to achieve the same performance twice as fast.

Communication objectives were to generate the highest awareness levels possible during the first few months of launching. Trial rates would also need to be very high within the first 3 months to generate sales ASAP.

c) Annual Media Budget

Confidential

d) Geographic Area

All major Canadian markets

Footnote 1: Nielsen MarketTrack – 4-week Period ending Nov 17, 2012

Footnote 2: Nielsen MarketTrack – 4-week Period ending Nov 17, 2012

Footnote 3: Nielsen MarketTrack – 4-week Period ending Nov 17, 2012

Footnote 4: Cassies Case Library, “Activia, three years of tasty success”, 2007, p.8

Section III — STRATEGIC THINKING

a) Analysis and Insight

The task Ultima was facing was daunting. But it also came with the opportunity to challenge all that had been done in the past and reinvent the way yogurt producers were communicating with the consumer. This strongly motivated the 30 marketing specialists of the Ultima team, and all communication experts involved. Passion for consumer knowledge pushed everyone forward with the desire to find new insights that would make iögo incredibly relevant to the consumers.

We met with over 4,000 Canadian consumers. We listened to them and tested our intuitions on every aspect of the marketing mix (brand names, brand architecture, positioning concepts, packaging design, product innovation, etc.).

From a product perspective, we quickly learned that we were heading in the right direction. Ultima’s choices were good and they suited the consumers’ demand. To stand out from the competition, we would develop a range of products that offered unique and original recipes with over 40 flavours, we would also shorten the list of ingredients by developing products that were gelatin-free and that had no artificial flavours or colours. iögo would be the first and the only major Canadian brand to offer a complete line of yogurts free of gelatin, colours or artificial flavours. Consumers wanted shorter labels and ingredients that they can understand—natural ingredients that require no explanation.

From a brand strategy perspective, we could not launch the new iögo line based only on product attributes and expect strong and sustained sales. These product differences are too easy to copy. We needed a distinct personality based on real values.

Before trying to define a distinct personality for iögo, we had to connect the brand to the company and people behind it. For 40 years, Ultima Foods had always referred to itself as Yoplait, never having questioned what defined the company as a manufacturer outside the Yoplait identity. We had to stand apart from everything we had done for Yoplait to find an new identity of our own.

After weeks of reflection on Ultima Foods’ identity, we came up with a deep emotional and powerful new brand story. Combined with an innovative and quality portfolio of products, this new brand story had what was needed to entice consumers to buy the new iögo brand.

“Ultima Foods is a company that is owned by the two most important Dairy Farmer cooperatives in Canada which represents more than 5000 Canadian Dairy farmers. And they are not willing to watch the business they built disappear. By launching iögo, these Canadian owners are taking a stand and calling out to Canadians to adopt a new high quality yogurt brand that stands for a strong collective and Canadian values.”

Since all major competitive yogurt brands are privately owned by multinationals, iögo was the only yogurt brand that had the authority to tell this particular kind of story. It now had an inspiring heritage and ideology of its own. Its motivation to sell yogurt was different from public companies listed on stock markets around the world. The cooperative values and the local ownership were aspirational and appealing. The special connection local farmers have with the food they produce, felt in touch with the choices people are making today. iögo was becoming a brand you could feel good about buying and be proud to adopt.

This was a call for mobilization. It’s the core idea that shaped the entire integrated communication strategy: communication to employees, to retailers, to the press and to consumers. This was not going to be another typical yogurt campaign.

All actions were aimed at making the most mobilizing launch ever—building proximity, trust, and emotions, through outstanding media visibility, while developing an attractive new personality. With this distinctive approach, a full portfolio of innovative products, a contemporary name, streamlined and appetizing packaging and a desire to break the codes in the yogurt category, there was no doubt in our minds that iögo would become the new way to say yogurt.

b) Communication Strategy

An appealing brand proposition and instant emotional impact was needed to build a successful launch campaign.

We created a marketing launch plan and a communication scenario that would attract the consumer to iögo. We needed to reach as many consumers as possible, get their attention, generate interest in the iögo brand. To do so, we placed an emphasis on resonating more deeply within consumers’ minds to motivate them to take action right away.

Again, an intensive period of consumer research interviews was conducted during strategic and conceptual development. Consumers told us they were connecting with the brand story. This was not just another yogurt ad falling in the clichés of supermodels eating yogurt, or presenting yogurt as modern medicine instead of food. The following quotes are from the consumers we spoke with: [Footnote #5]

‘Other ads focus on the yogurt. But iögo tells me something about the company. It’s refreshing and different.’

– Jenny, yogurt consumer, Toronto

‘iögo talks about things other companies do not. They’re not pushing it on you. Instead, they’re saying : ‘Here’s what we’re about. We believe in ourselves and let you make your choice.’’

– Paula, yogurt consumer,Toronto

The communication insights we had identified were clearly giving us an edge over the competition. The connection with people iögo developed was taking place way above functional and nutritional benefits. This was very encouraging.

Footnote #5 – Ad hoc research, Focus Groups conducted in 2011

Section IV — KEY EXECUTIONAL ELEMENTS

a)Media Used

A perfectly coordinated, integrated campaign aimed at employees, trade, influencers and consumers was put into place. The contact points we used to reach consumers were simple but very effective:

Week of August 13, 2012: Making consumers curious about something new called iögo

Television: 5 second teasers

Out of home advertising: Billboards, super-boards, bus shelters, and oversize posters during the Roger Cup tournament in Montreal and Toronto.

Starting week 2: The iögo storytelling

Television: 60-second anthem commercial

Out of home advertising: Billboards, super-boards, bus shelters

PLUS subway stations, skytrains, homepage takeovers on the web, magazine ads and a newspaper ad with a high-value coupon

Starting week 5 until mid November: Getting familiar with iögo’s product lines

Television: Seven 30-second commercials

Out of home advertising: Billboards, super-boards, bus shelters

b)Creative Discussion

‘iögo’. A memorable short name. Totally different from competitors. And consumers clearly appreciated the graphic allure of the umlaut (two dots) on top of the name.

Although looking at the brand name one could think that the two dots over the ‘O’ made it more Scandinavian than Canadian. So we decided to take the bull by the horns and make this problem a driving force. The creative approach transformed the exotic dots into a strong high-profile branding icon. In our brand stories, iögo lovers, iögo fruit flavours and products would be accompanied by the differentiating dots of the brand name.

The creative approach felt contemporary, democratic and modern, setting iögo apart from all other traditional brands. Its refreshing tone and graphic design made it stand out and gave it a leadership aura. The casting – real down to earth people – made the brand authentic and close. The entrepreneurship of the farm owners connected the brand with Canadian consumers coast to coast. Add simple to understand product attributes, and there it was: iögo, the new category challenger.

c)Media Discussion

The idea was to get the campaign noticed and create some buzz around town. We wanted people to talk about iögo. Three guidelines led the media strategy.

1- Be unexpected. Get the consumer curious from day one.

2- Keep the media mix simple, and maximize every media we use (high reach/frequency).

3- Media selection and environments must magnify the impact of our visual communications.

In August 2012, the campaign went live with its impressive visuals, unusual sizes and shapes. Our media presence was something never before experienced in the category. It was surprising. A 1-week “teaser” phase composed of 5-second TV spots and billboards preceded the official launch. High media frequency, and having fun with the two dots in unbranded advertising executions teased the consumer. Working closely with national outdoor media networks, we managed to have 80% of all outdoor posters installed within 2 days across Canada!

In the following weeks, fully branded high-impact executions quickly followed in impactful medias: subway stations, skytrains, 60-second and 30-sec TV commercials, billboards, and homepage takeovers on the web. Multiple creative ads were used across all mediums. Furthermore, the marketing program dovetailed perfectly with advertising efforts, adding more contact points with the consumer (web, social medias, public relations, stunts, in-store advertising and sampling in major events). The word ‘iögomania’ was used in social media to describe the intensity that the marketing communications activities were generating. Even journalist got caught in the ‘iögomania’. Some headlines were bringing even more attention to our campaign: ‘You must have been hiding under a rock if you haven’t noticed iögo’.

Section V — BUSINESS RESULTS

a) Sales/Share Results

The consumers’ response to the launch campaign was beyond our expectations.

According to Nielsen, trial levels skyrocketed, and iögo achieved a 9.6% market share after only three months. And results were even more encouraging looking at our performance in the Fat-Free yogurt category. In this high volume but stagnant category, iögo managed to steal up to 19.9% of the market, in relation to Source and Silhouette, and was now in a position to challenge Silhouette’s second place standing. [Footnote #7]

When comparing iögo’s launch to Activia’s in 2004, it becomes obvious how fast iögo was able to grab an important piece of the yogurt market. As Chart I demonstrates, iögo achieved in three months higher sales levels than Activia did in 2 years! Not to mention that Activia’s Marketing Strategy had proven its effectiveness in other countries before Danone introduced it in Canada. [Footnote #8]

Awareness levels have boomed in the same way. After only 3 months of being on the market, iögo achieved a national awareness rate of 74% among yogurt consumers, which is far beyond industry norms (3-month awareness norm is 32%, according to Ipsos). Awareness levels rose at a pace rarely seen according to Ipsos: the 32% national awareness benchmark was achieved after only 2 weeks. [Footnote #9]

The campaign was highly persuasive as these motivation indexes show: ‘The ad made you want to buy the brand’ (index of 244 vs norm), ‘The ad increased your interest in the brand’ (index of 243 vs norm). [Footnote #10]

Our goal for the launch of iögo was to make noise, introduce ourselves, get people talking about us, encourage them to try our products, and adopt our brand. So far, so good.

In the same 3-month period, the launch campaign generated word of mouth and press visibility: 133 press releases for a potential outreach of 40 million views. Also, 4392 mentions in social media (3427 on Twitter alone) for a potential outreach of 5 million views. Our Facebook page reached 40,000 fans.

For its accomplishments iögo won numerous national and international prizes in numerous fields such as product innovation, project management, packaging design, brand strategy, PR awards and many more.

b) Consumption/ Usage Results

c) Other Pertinent Results

d) Return on Investment

Footnote #7: Cassies Case Library, «Activia, three years of tasty success», 2007, p.8

Footnote #8: Nielsen MarketTrack – 4-week Period ending Nov 17, 2012

Footnote #9: Ipsos ASI advertising post tracking, 2012

Footnote #10: Ipsos ASI advertising post tracking, 2012

Section VI — CAUSE & EFFECT BETWEEN ADVERTISING AND RESULTS

a)General Discussion

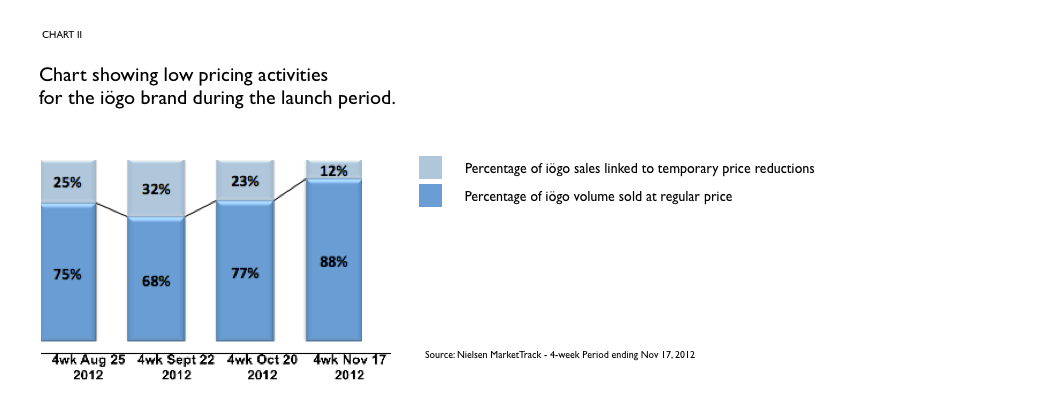

Nielsen MarketWatch sales charts clearly indicate that the timing of advertising efforts perfectly matches sales progression. But what’s more interesting is Chart II, presented below. It shows the relative importance of price cuts on sales during our 3-month launch period. We see that the 9.6% share of market iögo achieved in only three months wasn’t dependent on price incentives. As a matter of fact, iögo’s market shares continued to grow as price incentives on iögo products were diminishing! Therefore, knowing that national distribution levels of iögo were relatively stable during this same period, we can conclude that sales results can be linked back to advertising effectiveness. [Footnote #11]

Furthermore price reduction activities for iögo were low compared to those of the competitors. During our launch period, Danone, Yoplait and Astro (Parmalat) volumes were sold at higher rates of discounted prices. [Footnote #12]

b)Excluding Other Factors

Spending Levels:

Spending levels were set to meet the category leaders’ share of voice.

Pricing:

As been demontrated in previous section.

Distribution Changes:

As been demontrated in previous section.

Unusual Promotional Activity:

As been demontrated in previous section.

Other Potential Causes:

Category growth :

As of 2009, annual growth in the yogurt sector fluctuated between 4.6% and 5.2%, and rose to 6.9% in fall 2012. Keep in mind that iögo launched in mid-August 2012. Research shows iögo had an impact on category growth.

Footnote 11: Nielsen MarketTrack – 4-week Period ending Nov 17, 2012

Footnote 12: Nielsen MarketTrack – 4-week Period ending Nov 17, 2012